The depreciation process is essential for the financial and tax management of companies. Through depreciation, companies can spread the cost of fixed assets over their useful life, which helps to reflect the wear and tear of assets and facilitates tax planning. In this article, we explore the most commonly used methods for calculating depreciation, including details about the formulas and how they apply in different contexts.

Depreciation method: Straight-line method

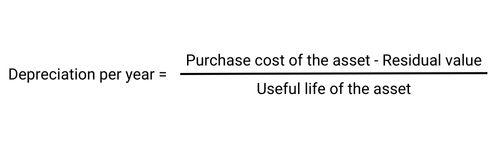

The straight-line method is the simplest and most commonly used in all types of companies. Its main characteristic is that it distributes the cost of the asset evenly over its useful life, regardless of changes in its use or productivity.

Calculation of annual depreciation:

In this case, the residual or salvage value represents the amount the asset is expected to be worth at the end of its useful life, although this data is not always required. The useful life varies based on the type of asset and the fiscal regulations of the country in which the business operates. Some examples include:

- Machinery, furniture and transportation (ships, trains, airplanes): 10 years.

- Vehicles and computer equipment: 4 years.

- Real estate: 20 years.

The residual value is not mandatory in all cases, but should be considered if the final value of the asset is to be reflected.

Advantages of the straight-line method:

- Simplicity: It is very easy to calculate and understand, making it a popular choice for small and medium-sized companies.

- Predictability: Depreciation is constant throughout the useful life of the asset, which facilitates financial planning.

Disadvantages:

- It doesn’t reflect the actual wear and tear of some assets: In some cases, such as technological equipment, depreciation may be faster in the early years, which the straight-line method doesn’t take into account.

Depreciation method: Sum-of-the-Years’-Digits

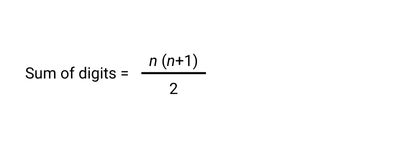

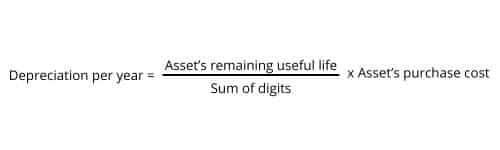

The sum-of-the-digits method is an accelerated approach that allows for greater depreciation in the early years of the asset’s life. This method is useful for those assets that lose their value rapidly after being acquired. The key to this method is that depreciation is distributed unevenly, with a higher percentage in the early years and less in the later years.

Formula of the sum of the digits:

Where n is the useful life of the asset in years. Then, the annual depreciation for each year is calculated as:

For example, if an asset has a useful life of 5 years, the sum of the digits would be 1+2+3+3+4+5=151 + 2 + 3 + 4 + 5 = 151+2+3+4+5=15.

This implies that the asset will depreciate at a faster rate during the first few years.

Advantages:

- Accelerated depreciation: This method better reflects the value of assets that lose their value rapidly, such as machinery or vehicles.

- Tax benefits: Since depreciation is higher in the early years, it can reduce the tax burden in the early stages of the asset’s useful life.

Disadvantages:

- Complexity: Requires more detailed calculations and can be difficult to apply compared to the straight line method.

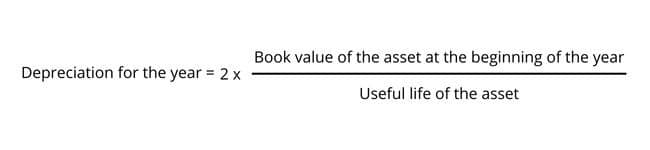

Accelerated depreciation method

The accelerated depreciation method allows assets to depreciate faster, recovering a larger portion of their value in the initial years. This approach is mainly used in tax situations where companies want to reduce their taxes quickly.

There are several ways to calculate accelerated depreciation, such as the double-declining balance method, but in general, the idea is for the asset to lose value more quickly in the early years.

Double declining balance formula:

Tax and financial advantages:

- Tax reduction: In the early years, the company can deduct a larger amount for depreciation, which reduces the tax base and, therefore, taxes.

- Improved cash flow: Accelerated depreciation allows for a higher initial tax deduction, which can improve the company’s cash flow.

Disadvantages:

- Impact on financial results: Although the tax impact may be positive, this method may distort financial results, as it does not reflect the real value in use of the asset.

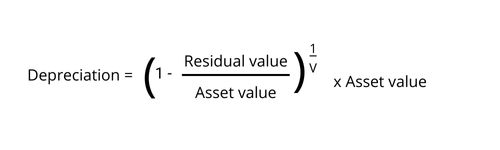

Declining balance method

The declining balance method is another type of accelerated depreciation, but with a slightly different approach. Here, the depreciation rate is calculated using the asset’s residual value.

Declining balance formula:

Where V is the useful life of the asset.

Advantages:

- More realistic reflection of asset wear and tear: This method is more suitable for assets that lose value rapidly due to obsolescence or heavy use.

- Favorable in tax terms: Like other accelerated methods, it allows higher tax deductions in the first years.

Disadvantages:

- It requires complex calculations: This method can be more difficult for companies to apply and follow, especially if they have many assets on their balance sheet.

Depreciation method: Units-of-Production

The units-of-production method is ideal for assets whose value is affected by their use or production, rather than elapsed time. This method is common in the manufacturing industry or in companies that operate specialized machinery.

In this case, depreciation is calculated by dividing the value of the asset by the total number of units it is expected to produce over its useful life. It is then multiplied by the number of units produced in each period.

Formula:

Each production period has a depreciation proportional to the number of units produced.

Advantages:

- Accuracy in assets with variable production: This method is perfect for assets whose wear and tear depends directly on their use, such as machinery in factories.

- Increased accuracy in measuring depreciation: Helps to more accurately reflect asset wear and tear.

Disadvantages:

- Tracking complication: A detailed record of production needs to be kept, which can be more complex and requires an accurate accounting system.

Take advantage of the best tax opportunities with our personalized advice.

The calculation of depreciation is a critical part of accounting and tax management for businesses, especially for those with significant fixed assets. Knowing the types of depreciation and the methods to calculate depreciation is essential for proper financial and tax planning. By choosing the appropriate method, companies can optimize their tax strategy and accurately reflect the value of their assets over time.

It is advisable to consult with specialized tax or accounting advisors, especially if your company has international operations or plans to establish itself in markets with complex tax regulations, such as Spain. Professional advice will allow you to make informed decisions and ensure that your company complies with all tax regulations while taking advantage of the best opportunities for tax savings and profitability. Do not hesitate to contact our tax advisory for personalized support that will boost your company’s financial management.