The contribution for salaries above the maximum contribution base increases

Starting January 1, 2025, employees earning above the maximum contribution base will see an increase in their contribution amounts, which will reduce their net take-home pay. Likewise, employers will also face higher costs for these employees, as this additional solidarity contribution affects both the employees’ and employers’ contribution quotas.

For 2025, the maximum contribution base has been set at €4,909.50, and this additional solidarity contribution will apply to remuneration exceeding this maximum base.

On March 17, 2023, Royal Decree-Law 2/2023, dated March 16, was published in the Official State Gazette (BOE), amending the General Social Security Law by adding Article 19 bis and an Additional Provision Forty-Second, with the following wording:

“Article 19 bis. Additional Solidarity Contribution

The portion of remuneration exceeding the maximum contribution base established for employees under the Social Security system will be subject, in all quota settlements, to an additional solidarity contribution. The solidarity contribution will result from applying a rate of 5.5 percent to the portion of remuneration between the maximum contribution base and up to 10 percent above it, a rate of 6 percent to the portion of remuneration between 10 percent and 50 percent above the maximum base, and a rate of 7 percent to the portion of remuneration exceeding 50 percent above the maximum base. The distribution of the solidarity contribution rate between employer and employee will maintain the same proportions as the general contribution rate for common contingencies.”

“Additional Provision Forty-Second. Implementation of the Additional Solidarity Contribution

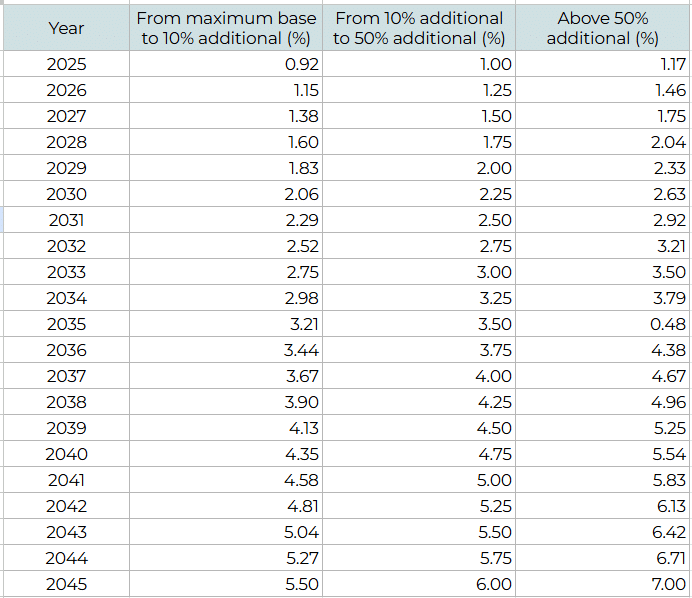

The additional solidarity contribution referenced in Article 19 bis will be applied to each bracket of remuneration exceeding the maximum contribution base, using the following percentages, expressed annually, from 2025 to 2045.”

The distribution of solidarity contribution rates between employer and employee will follow the same proportions as the general Social Security contribution rates for common contingencies.

The percentages established in Article 19 bis will be the definitive rates applied starting in 2045. However, the Additional Provision Forty-Second establishes a gradual implementation of these rates beginning in 2025. For 2025, the applicable percentages are as follows:

For the distribution of these percentages between the employee and the employer, we refer to Article 17 of the Contribution Order published on December 3, 2024, which specifies the details:

“The solidarity contribution will result from applying a rate of 0.92 percent to the portion of remuneration between €4,909.50 and €5,400.45, with 0.77 percent paid by the employer and 0.15 percent by the employee; 1 percent applied to the portion of remuneration between €5,400.46 and €7,364.25, with 0.83 percent paid by the employer and 0.17 percent by the employee; and 1.17 percent applied to the portion of remuneration exceeding this amount, with 0.98 percent paid by the employer and 0.19 percent by the employee.”

In summary, for 2025, the additional solidarity contribution is divided into the following brackets and percentages.

Three important points to keep in mind:

- The amounts resulting from the application of these percentages cannot be subject to any type of bonus, reduction, exemption, or deduction.

- This additional contribution applies to all types of settlements. This means it is applied to both regular remuneration and retroactive payments, bonuses, variable remuneration, etc., as long as they are earned starting January 1, 2025, regardless of the payment date.

- This additional contribution does not provide any benefits for the affected employee, as it is a system of contribution to the pension fund but does not increase their contribution base. Regardless of the increase in the contribution for these employees, their contribution base will remain at €4,909.50.

Additionally, it is important to remember that, in compliance with Law 21/2021, which established the Intergenerational Equity Mechanism (MEI) starting in 2023 with gradual implementation until 2032, the MEI percentages for 2025 are as follows:

- Employee’s share: 0.13%

- Employer’s share: 0.67%

- Total: 0.80%

Finally, starting January 2025, payrolls will detail the amounts corresponding to the Intergenerational Equity Mechanism and the Additional Solidarity Contribution, showing both the employee’s and employer’s contributions. However, if an employee falls into multiple brackets for the Additional Solidarity Contribution, the payroll will reflect a single line with the total amount.

We can help you apply the additional solidarity contribution increase

If you need support to implement this change in your company, we offer a payroll services in Spain that ensures compliance with regulations and the correct application of the new contributions. Don’t hesitate to contact us for more information.